BRSR – Raises the Bar for ESG disclosures in India

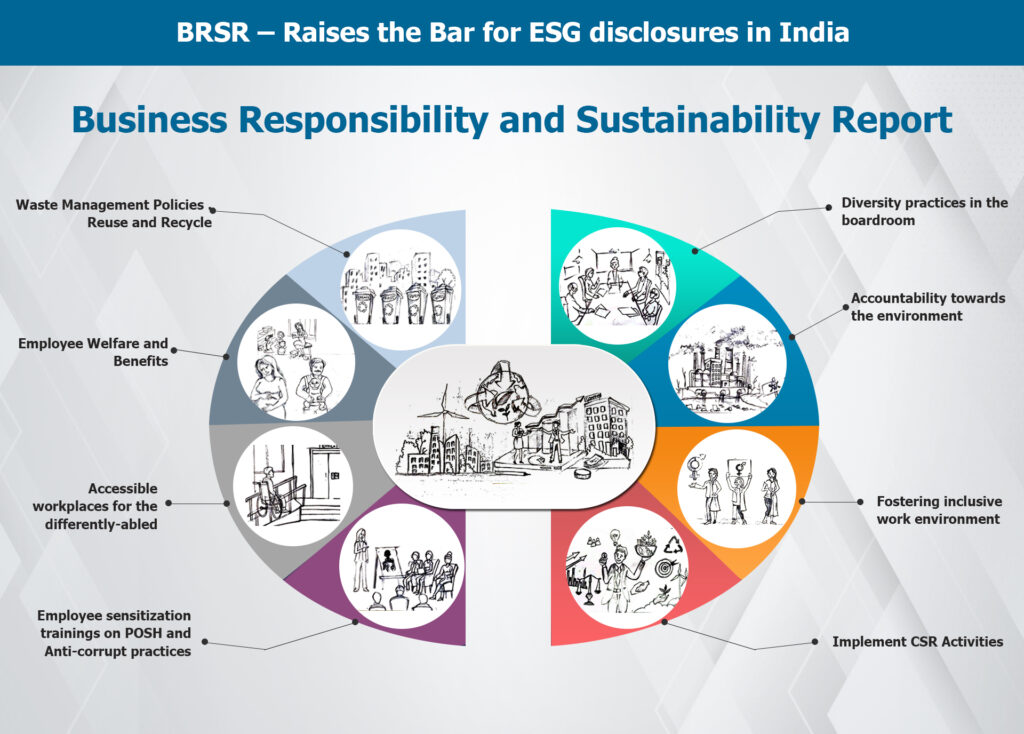

Effective FY 2022-23 onwards, the Top 1000 listed companies (by market capitalization) in India will be mandatorily reporting out their Business Responsibility and Sustainability Report (BRSR). However, this is not the first-time companies will be making disclosures about their responsibilities and sustainability initiatives. The foundation stones of implementing ESG in India goes back to the year 2009 when Ministry of Corporate Affairs (MCA) issued the Voluntary Guidelines on Corporate Social Responsibility which stood revised to the National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business (NVG) in 2011. Thereafter, in 2012, Securities and Exchange Board of India (SEBI) mandated the Top 100 listed entities (by market capitalization) to file the Business Responsibility Report (BRR) based on the NVG principles and extended the mandate of filing BRR to the Top 500 listed entities (by market capitalization) in 2015 which got further extended to the Top 1000 listed entities in 2019. In 2019 MCA updated the NVG guidelines to National Guidelines on Responsible Business Conduct (NGRBC) to factor global developments and national changes which led to SEBI introducing BRSR in 2021 to align it with the NGRBC by not only enhancing the number of disclosures but also requiring evidence-based data. BRSR is expected to provide meaningful insights into a company’s performance on non-financial parameters to all its stakeholders and evaluate a company’s accountability towards the environment, complying with the regulatory framework, ensuring bias-free and safe workplaces, diversity practices in the boardroom, promoting human rights, fostering inclusive work environment, striving towards corruption free work ethics, making workplaces accessible to the differently abled etc.

It is important to emphasize upon the guidance document accompanying BRSR which facilitates understanding the disclosures better and in turn helps one to fill up the requested data accurately. It must be read in consonance with BRSR and not as a standalone Annexure. A few aspects which get clarified in the guidance document is as follows:

For disclosures which may not be applicable to certain type of industries, entities can mention that such disclosure is not applicable to them citing reasons for the same. For example, Principle 6 of BRSR requires entities to disclose details about the mechanism for zero liquid discharge, air emissions, greenhouse gas emissions etc. For instance, a non-manufacturing industry which does not have any liquid discharge and air emissions but fall in the bracket of companies which need to mandatorily file the BRSR, can opt to write ‘not applicable’ giving the reasons against these disclosures.

The guidance document clarifies how to calculate percentage/number for certain quantifiable disclosures.

It clarifies on the inter-operability of the reporting framework such that the entities which are doing sustainability reporting as a part of their annual report basis internationally accepted reporting frameworks like Global Reporting Initiative, Sustainability Accounting Standards Board, Task Force on Climate-related Financial Disclosures, and Integrated Reporting can cross-reference their disclosures that they have made under these formats to the disclosures that are required in BRSR. This will avoid the companies to do duplicate reporting in the annual report. The companies must ensure that they have mentioned the specific page number of the annual report or the sustainability report which they are cross-referencing.

While at the first glance BRSR may seem like an arduous disclosure framework requiring a fair number of datapoints, what needs to be realised here is that these are not requirements which have been introduced for the first time. Majority of them are compliances emanating from existing enactments which companies are anyways required to adhere with such as those emanating from the Companies Act, 2013 and allied rules, Environment Pollution Act, 1986 read with the allied rules, Maternity Benefit Act, Workmen’s Compensation Act, Minimum Wages Act, Rights of Persons with Disabilities Act, 2016, to name a few. Hence, it would not be appropriate to think that way too many disclosures have suddenly been thrust upon companies. Further, listed companies have been making several public disclosures as a part of their corporate governance mandate for the past couple of years under the SEBI regulations. Having a robust compliance management system in place is becoming more of a necessity for the organizations. We have noticed several steps taken by the government by way of enacting new law / amending existing laws which have gone a long way in paving the path to adopt a robust disclosure framework like the BRSR. To name a few, we noticed the Companies Act, 2013 prescribing the requirement for certain classes of companies to have women directors on their board to address gender gaps in governance; the board report mandating a statement on compliance relating to the constitution of an Internal Committee under the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013. In the year 2018, we noticed SEBI going ahead and stipulating the Top 1000 listed entities to mandatorily have a woman independent director on its board.

A couple of human rights centric legislations were enacted over the years such as the Rights of Persons with Disabilities Act which got notified in the year 2016 and what is worth mentioning is that several obligations emanating from this Act are being sought as disclosures in BRSR such as whether the premise/office of the entity is accessible to differently abled employees/workers/ visitors, and if not, whether any steps are being taken by the entity in this regard. BRSR also questions whether the entity has an equal opportunity policy and if it does then a web-link to the policy. Also, details on the number of permanent and other than permanent differently abled employees and workers.

In the year 2019, the Transgender Persons (Protection of Rights) Act was enacted to ensure equal treatment of transgender persons in matters of employment, infrastructure adjustments, recruitment, employment benefits and other related issues. Interestingly, the guidance notes, which is a part of BRSR clarifies that in disclosures relating to gender, BRSR specifies male and female while seeking information related to gender ratio/wages etc. However, if an entity has employed persons who have not disclosed their gender or belong to any other gender, a separate column of “Other” may be added for such disclosures.

What is pertinent to mention here is while the Indian law currently does not mandatorily require companies to hire transgender and / or differently – abled persons, BRSR requires disclosures around them that too as a part of its Essential (mandatory) indicators.

What we observe is that the BRSR improved upon the BRR by requiring quantitative disclosures in addition to qualitative disclosures. BRSR requires enhanced transparency and is a rigorous report. The BRR is more a tick in the box reporting whereas, BRSR is a data driven and evidence-based reporting framework. Just to explain this better let’s take the women director requirement as an example. While BRR has not specifically required information on women directors in the report, BRSR specifically demarcates placeholders to key in information on percentage of females in the company’s Board of Directors (“BOD”) and / or Key Managerial Personnel (“KMP”) and the median remuneration/salary/wages separately for male and female in respect of the categories BOD, KMP, workers, employees other than KMP and BOD.

Further, while BRR merely mentions as a part of its Principle 3 that businesses should take cognizance of the work-life balance of its employees, especially that of women and should provide facilities for the well-being of its employees including those with special needs, BRSR has taken it ahead and ascribes metrics around it by requiring companies to key in data on the percentage of employees covered by maternity benefits, paternity benefits, day care facilities etc., requesting data separately for male and female employees. What is interesting to note here is that though India has not yet enacted a law on granting paternity benefit, BRSR requires information on it. Further, the guidance note on BRSR also encourages to add more well-being benefits apart from the benefits mentioned in BRSR given by the companies, if any. It is important to highlight that, while providing a crèche facility was mandated by the Maternity Benefit Act back in 2017, owing to failure on the part of States to come up with the complementary State rules on this requirement, day care facilities too may not have been set up by several companies yet. However, we see Principle 3 of the BRSR format requiring companies to disclose data on the day care facilities as well and this brings us to the conclusion that there are certain disclosures for which companies might not be prepared now but may need to start putting in place to be able to fair well on these parameters too.

Principle 1 of BRSR requires companies to make disclosures with respect to training and awareness programmes done on the principles by the companies. Thus, the companies should now ensure that they are imparting the necessary trainings and awareness programmes which cover the principles.

Principle 5 of BRSR requires companies to disclose percentage of employees to whom they have paid wages equal to minimum wage and percentage of employees to whom they have paid more than minimum wage. As per the present law, the Minimum Wages Act lays down that companies must pay the minimum wage.

What we discussed so far is not the exhaustive list of disclosures which companies can/should undertake to report BRSR efficiently. We have picked up a few amongst the huge number of disclosures it requires. As we mentioned earlier in this blog, most of the number of disclosures BRSR requires is statutorily required to be done by the companies anyways and are monitored on a regular basis. Law already mandates maintenance of certain disclosures in the form of registers, returns, books, etc. from where several data points required in BRSR can be obtained. Having said this, there are few disclosures (some of which we discussed earlier in this blog) which companies will need to do over and above the requirement flowing from any law presently as a ‘good to have’ to be ready for BRSR reporting. Companies should start preparing for BRSR by collating the required datapoints from their business units and their supply chain, recalibrate what it needs to bring in place, mould operations basis the reporting requirements etc. While the changes required may cost the companies in the short term, however, in the long run it would reap benefits for the companies by increasing the value creation, increasing access to capital, reducing financial risk, giving it a social license to operate, attracting and retaining talent, improving brand value and reputation, and instilling higher investor confidence. The enhanced disclosures required in BRSR is most certainly a step in the right direction to provide insights to all its stakeholders be it investors, shareholders, regulators, and the public at large to evaluate the principle-wise performance of a company and help investors make more informed investment decisions.

Lexplosion Solutions have been helping organizations across the globe to comply with the changes brought in by the regulations. In case you want to know more about how we can help you with your compliance management, particularly the BRSR requirements, get in touch with us now.

Written by: Pragya Saraf

Co Authored by: Antara Dasgupta

Disclaimer

All material included in this blog is for informational purposes only and does not purport to be or constitute legal or other advice. This blog should not be used as a substitute for specific legal advice. Professional legal advice should be obtained before taking or refraining from an action as a result of the contents of this blog. We exclude any liability (including without limitation that for negligence or for any damages of any kind) for the content of this blog. The views and opinions expressed in this blog are those of the author/(s) alone and do not necessarily reflect the official position of Lexplosion Solutions. We make no representations, warranties or undertakings about any of the information, content or materials provided in this blog (including, without limitation, any as to quality, accuracy, completeness or reliability). All the contents of this blog, including the design, text, graphics, their selection and arrangement are the intellectual property of Lexplosion Solutions Private Limited and/or its licensors.

ALL RIGHTS RESERVED, and all moral rights are asserted and reserved.

Lexplosion Solutions

https://lexplosion.in/Lexplosion Solutions Private Limited is a pioneering Indian Legal-Tech company that provides legal risk and compliance management solutions through cloud-based software and expert services.